Have you ever wondered how your company accounts for all that well-deserved Paid Time Off (PTO)? You know you grant it, and your employees use it, but what is the monetary value of the unused hours? That's where PTO Liability comes in.

It’s an important number for any business! Simply put, PTO Liability is the estimated dollar amount your company would owe employees for their unused PTO as of a specific date (usually the end of a reporting period). Think of it as a formal IOU on your balance sheet.

The Core Equation

Regardless of your specific GoCo policy setup, the fundamental calculation for PTO liability is:

PTO Liability = Total Unused PTO Hours x Employee’s Rate of Pay

The calculation's complexity only changes based on two factors: how time is earned and if it must be paid out.

1. How Time is Earned: The Two Types of Policies

The biggest factor in calculating liability is whether your policy is an Accrual or a Lump-Sum Grant.

⚖️ Scenario A: The Accrual Method (Earning Over Time)

In this common setup, employees earn small amounts of PTO with each pay period (e.g., 4 hours per bi-weekly paycheck).

The Liability Logic: You only accrue liability for the PTO an employee has actually earned up to the calculation date.

-

Use Case: Meet Alex. Alex is paid $25/hour. Their policy grants 4 hours of PTO per bi-weekly paycheck. On the date you run liability, Alex has only been with the company for 10 pay periods and has used no time.

-

The Math: (10 pay periods x 4 accrued hours) x $25/hour = $1,000 liability

| Component | Description |

| Unused Hours | Only includes the hours that have been accrued by the employee to date. |

| Rate of Pay | Typically the employee's current hourly wage or a standard rate defined by your finance team. |

🎁 Scenario B: The Lump-Sum Grant Method (Given Upfront)

In this setup, employees receive their full allotment of PTO (e.g., 80 hours) on their anniversary or the first day of the year.

The Liability Logic: You accrue liability for all hours granted—unless your policy specifies a proration or a "use it or lose it" clause that is legally enforceable.

-

Use Case: Meet Blake. Blake is paid $25/hour and was granted 80 hours on January 1st. On the date you run liability, they have used 10 hours.

-

The Math: (80 granted hours - 10 used hours) x $25/hour = $1,750 Liability

2. The Payout Rule: State Laws and the “Must Pay” Factor

This is the most critical piece that determines if the liability matters to your accounting team.

Your PTO liability calculation will only include time that is required to be paid out to an employee upon separation or termination.

-

If your company is in a state where PTO is considered earned wages (like California or Massachusetts) and must be paid upon termination, your full unused PTO balance is a legal liability and must be included in the calculation.

-

If your company is in a state that allows "use it or lose it" policies (and your policy is written that way), then the liability calculation will exclude time that an employee would forfeit upon leaving.

The GoCo Benefit: GoCo helps you manage these complex time-off balances accurately in your Time Off Settings. This ensures that the unused hours figure is precise, so your finance team can apply their specific payroll rates and state rules to complete the liability calculation.

How to Make Changes to Your PTO Liabilities

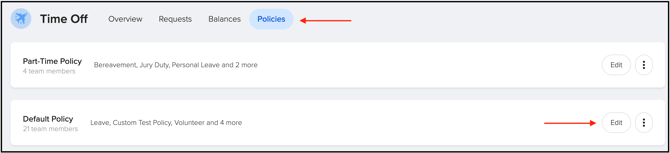

- Click on the Policies tab in your Time Off app. Then Edit on the policy you wish to make changes to.

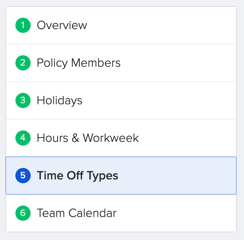

- Navigate to the Time Off Types Step, and then click Edit on the time off type you want to update.

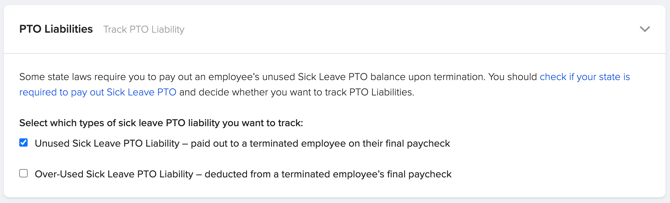

- Now we'll scroll down to the bottom of the page to find the PTO Liabilities tab and expand.

- Note: This is only available for Accrued Policy Types.

- From here you can select which types of PTO liability you want to track!

- Lastly, Save your Time Off Rules at the bottom right of the page

❓ Frequently Asked Questions (FAQ)

-

Is this different from my normal PTO reporting? Yes! Your standard PTO reports show balances and usage for HR; the liability report is a financial calculation for your accounting/finance team to comply with GAAP (Generally Accepted Accounting Principles).

-

What if an employee hits their PTO cap? If your policy has a cap, the liability calculation stops at that maximum number of hours. If an employee is capped at 120 hours, your liability is calculated based on those 120 hours (or less, if they have used some)

If you have additional questions please contact support@goco.io